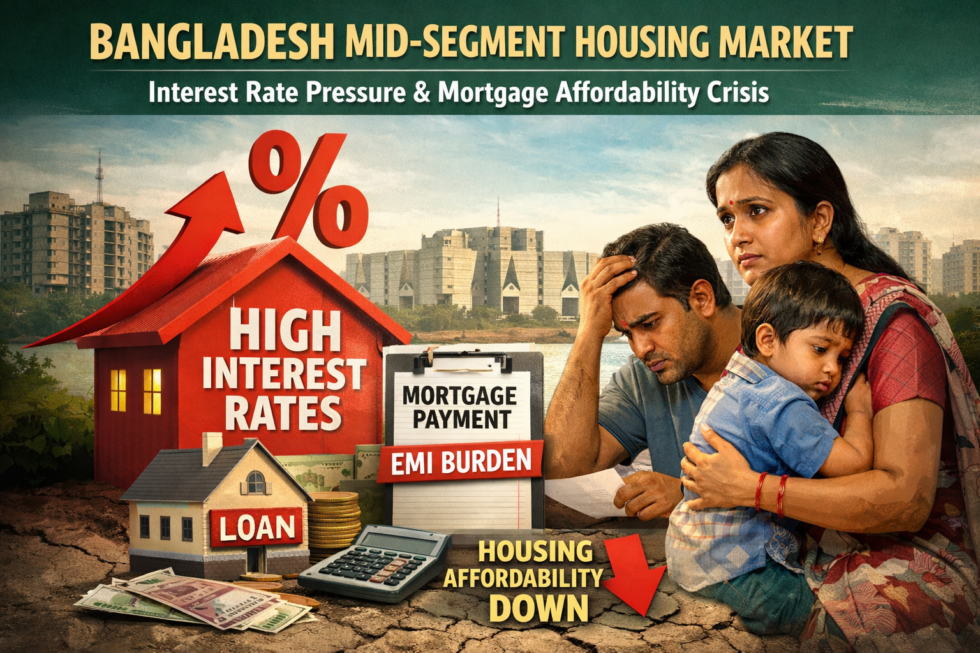

The development surrounding Bangladesh Mid-Segment Housing Market Interest Rate Pressure highlights the growing influence of borrowing costs on urban housing demand and mortgage affordability. The mid-segment housing category, which primarily serves middle-income households, is particularly sensitive to changes in financing conditions because most buyers rely heavily on bank loans to purchase apartments.

Recent reports indicate that rising interest rates are discouraging prospective buyers from committing to mortgage-backed purchases. As borrowing costs increase, monthly repayment obligations rise, reducing the number of households that can qualify for housing loans and delaying purchase decisions.

The resulting slowdown in apartment sales is extending inventory cycles for property developers and may increase financial pressure within construction projects that depend on advance sales and project financing. The situation illustrates how Bangladesh Mid-Segment Housing Market Interest Rate Pressure can transmit monetary tightening effects directly into real estate activity and construction sector dynamics.

Beyond property transactions, the slowdown may influence related industries including construction materials, housing finance institutions, and urban labour markets connected to real estate development.

Monitoring mortgage rate movements, apartment sales trends, and bank exposure to real estate lending will be important for assessing whether the current pressure represents a temporary adjustment or a longer-term shift in housing market financing conditions.

Why this matters

The mid-segment housing market plays a central role in Bangladesh’s urban real estate ecosystem. It sits between luxury developments and low-income housing and largely depends on mortgage financing and middle-income household purchasing power.

When borrowing costs rise sharply, this segment is often the first to slow. Higher interest rates reduce affordability for potential homebuyers and can delay purchase decisions, affecting property developers, construction activity, and housing-related industries. For financially aware readers, the slowdown signals broader implications for credit markets, construction demand, and urban economic momentum.

What has been reported

The Daily Star reports that rising borrowing costs are slowing Bangladesh’s mid-segment housing market. Developers say that higher loan interest rates are discouraging middle-income buyers who rely heavily on bank financing to purchase apartments.

The report indicates that many prospective buyers are postponing purchases due to the increased cost of mortgage loans. Developers are also facing slower sales and longer inventory cycles as financing becomes less accessible.

The coverage highlights that the pressure is particularly strong in the mid-income housing segment, where affordability depends significantly on bank loans and housing finance.

Structural implications beyond real estate sales

Housing markets are closely tied to broader financial conditions. When interest rates rise, the cost of mortgage financing increases, reducing the number of households able to qualify for housing loans.

The mid-segment housing market is especially sensitive because buyers in this category typically rely on loans rather than full cash payments. A higher borrowing cost therefore directly reduces demand.

At the same time, developers often rely on project financing or advance sales to manage cash flows. Slower apartment sales can extend project timelines and raise financial stress for construction firms.

Impact on related sectors

A slowdown in housing demand can affect several industries connected to construction and real estate development.

These include:

Construction materials such as cement and steel

Interior and finishing industries

Construction labour markets

Housing finance institutions and banks

Reduced property transactions can therefore ripple through multiple sectors of the economy.

Financing environment and affordability pressure

Interest rates in the banking system have increased as monetary conditions tighten. Higher rates translate directly into higher monthly mortgage payments.

For middle-income households, even small increases in loan interest rates can significantly affect affordability calculations. As a result, many buyers are choosing to delay purchases rather than commit to long-term loans under uncertain financing conditions.

If borrowing costs remain elevated for an extended period, the slowdown in the mid-segment housing market could persist.

Risk assessment

If borrowing costs stabilise or decline, housing demand may gradually recover as postponed purchases return to the market.

If interest rates remain high, developers may face prolonged inventory cycles and slower cash flow, which could delay new project launches.

A sustained slowdown could also influence bank lending patterns to the real estate sector.

What to monitor next

Interest rate trends in housing loans

Apartment sales volumes in urban housing projects

Construction sector activity indicators

Bank lending to real estate developers and homebuyers

Policy signals related to housing finance or mortgage support

Neutrality and disclosure

This report is prepared for analytical and informational purposes only. It does not constitute investment advice. The analysis is based on publicly reported information.

Sources referenced

The Daily Star

Rising borrowing costs stall mid-segment housing market

https://www.thedailystar.net/business/economy/news/rising-borrowing-costs-stall-mid-segment-housing-market-4112466

Institutional Lens

From an institutional perspective, Bangladesh Mid-Segment Housing Market Interest Rate Pressure reflects the transmission of tighter monetary conditions into mortgage-dependent real estate demand. Analysts will primarily evaluate how rising borrowing costs affect housing loan eligibility, developer sales cycles, and bank exposure to residential property financing. The mid-segment housing category is particularly sensitive because purchase decisions rely heavily on credit availability rather than cash transactions. Institutions will monitor whether slower apartment sales translate into extended project timelines, rising developer leverage, or adjustments in bank lending policies toward real estate and housing finance.

Retail Perception Lens

For retail participants, Bangladesh Mid-Segment Housing Market Interest Rate Pressure is often experienced through affordability calculations rather than broader credit market conditions. Higher mortgage rates increase monthly loan repayments, which can alter household purchase decisions and delay homeownership plans for middle-income buyers. Even moderate increases in interest rates can significantly change loan eligibility thresholds. As a result, many prospective buyers may adopt a wait-and-see approach until borrowing costs stabilise. Retail perception in this segment is therefore closely linked to mortgage affordability rather than overall real estate price dynamics.

Governance-Focused Perspective

From a governance standpoint, Bangladesh Mid-Segment Housing Market Interest Rate Pressure raises questions about the resilience of housing finance frameworks and banking sector exposure to property lending. Policymakers and financial regulators may examine how rising interest rates influence credit allocation, developer financing structures, and mortgage accessibility for middle-income households. Governance analysis will also consider whether prolonged affordability pressure could alter lending patterns within the banking system or increase risk concentrations in real estate-related portfolios. Transparent monitoring of housing finance trends therefore becomes essential for maintaining financial system stability.